Convenience Store News recently published its 2024 Technology Study. The “Loyalty, Apps, & Payment Tech” section piqued my interest. Let’s start with loyalty.

Face it: the job of a loyalty program is to give people a reason to visit more often. Loyalty is the ambition to give someone a reason to take a left-hand turn into your store when the competition is on the right (or the reverse for those of you in regions that drive on the left). This is why nearly all large c-store operators have at least one, if not several, loyalty programs and schemes. More than four out of five of these programs can be accessed through a mobile app, with just under half (44%) going mobile app only (no website or other access point).1

Look, ma – no website!

This makes sense, when you think about it. C-store trips are usually spontaneous, unplanned affairs. However, just because you hit the sweets aisle doesn’t mean that any sweets aisle will do. Mobile apps fit the bill by providing store locations, limited-time specials, vendor coupons, customer feedback, fuel prices, and personalized/targeted offers. This is a good start, but it leaves money on the table. Less than one-third (30%) of these apps incorporate points/rewards and a payment card or other option.2

The market recognizes the value of in-app payments and plans to adopt them – nearly 40% aim to add mobile payments to their apps, while 44% plan to offer mobile ordering. Among large chains, this rises to nearly three-quarters of those surveyed.3

What is “loyalty leakage?” I’m glad you asked!

C-stores benefit from effective mobile app payment programs, which prevent loyalty leakage. Loyalty leakage happens when a purchase isn’t linked to a loyalty account, losing valuable data for the merchant and recognition for the customer. C-stores can link payment cards to loyalty accounts via their app using tokenization, recognizing and rewarding customers automatically without needing an additional swipe. With a little bit of orchestration, this technique can pay huge dividends. Consider the average fueling transaction. Once a card payment is authorized, the consumer will be at the pump for about five minutes. A smart merchant can quickly identify a loyalty member (via the payment card token) and send an appropriate offer to their phone (via SMS or push) in those precious five minutes, driving them into the store. Realizing that a C-store’s number one product is, in fact, convenience, let’s go one step further. Suppose that a text message or push notification provides a link to a personalized online “pop-up” store that offers the consumer in-store items that can be purchased instantly and brought to them at the forecourt. Convenience is king, indeed!

How easy is it to add in-app payments?

Most payment service providers will have a software development kit (SDK) to tie their existing payments system into the app. At ACI, our mobile SDK (mSDK) enables payments quickly in mobile apps.

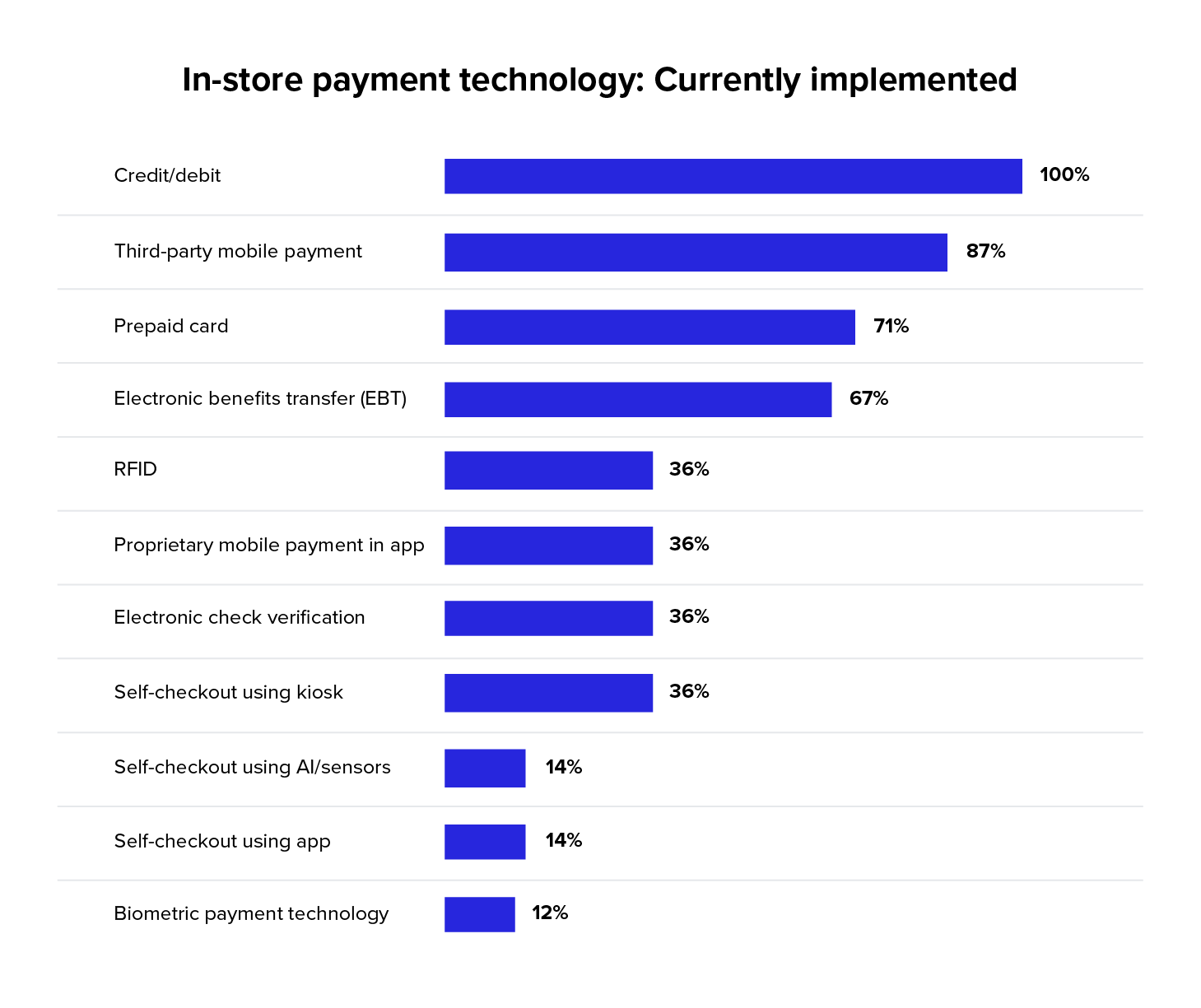

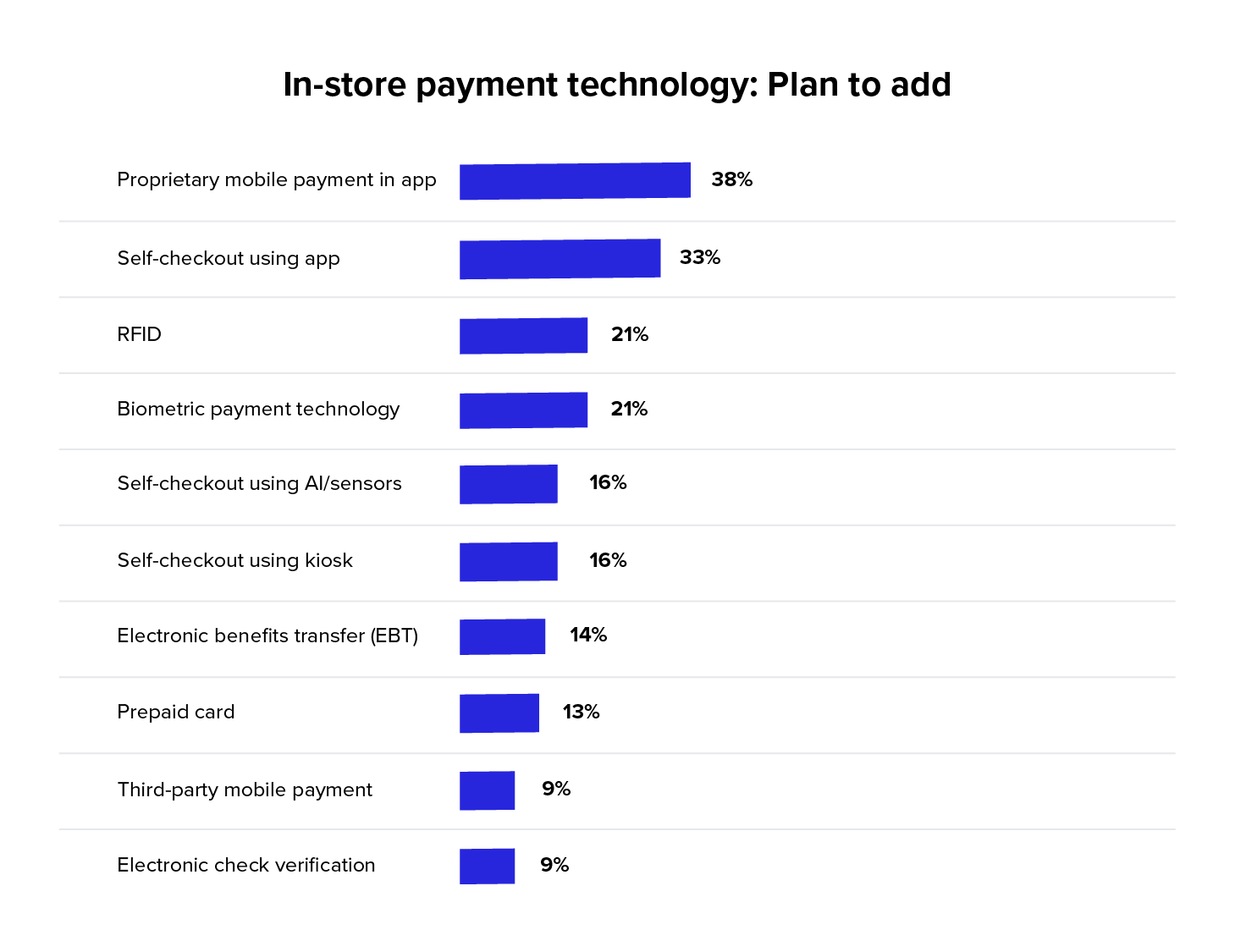

What payment types are C-store merchants planning to implement in-store?

The survey results indicate a substantial demand for more self-checkout options. Notably, half of the top six survey responses involve self-checkout using various methodologies, with one-third of participants planning to use an app-based self-checkout system, surpassing the combined total of the other methods.4 This trend aligns with our previous discussions. Additionally, proprietary mobile payment within apps is preferred by nearly 40% of respondents,5 underscoring the importance of convenience and loyalty in payment options.

Biggest changes from 2023 to 2024

Prepaid card acceptance increased from less than 50% in 2023 to nearly 75% in 2024.6 Conversely, self-checkout AI/sensors and kiosks experienced a significant decline, likely due to immature technology, high costs, and complexity.

What about the forecourt?

Nearly a quarter of respondents cited mobile app payments, in-car payments, and RFID as the top planned forecourt payment options.

Vehicle manufacturers face challenges with in-car payments, such as competing for screen control on infotainment systems and dealing with standardization issues. Technological hurdles also exist. For example, U.S. fuel stations with multiple pumps per lane make it hard to identify which vehicle corresponds to which dispenser. Solutions like entering a pump number or code add friction, making card or phone payments preferable because customers have to exit their vehicles to fuel anyway.

Overall, the study gives hope for advancements at the C-store, but in many ways, it raises nearly as many questions as it answers – for example, the data does not factor in regional variations (i.e., cold weather climates may increase demand for in-vehicle payments vs. more temperate areas).

As far as bang for the buck and ROI are concerned, utilizing mobile devices for payments, loyalty and timely offers would be the best place to concentrate efforts. In particular, linking loyalty and payments in your mobile app is the best strategy for C-store merchants in 2025.

Dan Coates is a senior solution consultant focused on payment solutions for merchant retail in the card present, eCommerce and mCommerce space. Dan has over 15 years of experience in payments, including leading payments systems implementation for a major petroleum retailer, writing and developing payments software for ACI’s omni-commerce platform, implementing large scale projects for many top global brands, and presenting new and exciting solutions to ACI’s current customers and companies around the world.

CustomersPartners

CustomersPartners