By far the world’s largest real-time player, India dominates the global real-time payments space with almost 130 billion real-time payments made in 2023. To put this in context, that’s more than the rest of the world’s top 10 real-time payment markets combined and 49% of total global real-time transactions.

India’s initiatives to empower merchants and consumers to reduce their reliance on cash range from no-fee accounts and digital IDs to pervasive QR codes and mobile wallets — all of which have paved the way for UPI real-time payments and made them ubiquitous in daily life.

India’s real-time journey began with the launch of Immediate Payment Service in 2010, but the game changer was the introduction of the Unified Payments Interface (UPI) in April 2016, which enabled real-time payments using QR codes, mobile numbers and virtual IDs.

UPI has made India the world’s #1 real-time payments market

UPI was developed by the National Payments Corporation of India (NPCI), which was established by the Reserve Bank of India (RBI) and the Indian Banks Association. Thanks to demonetization mandates and opening the system to non-bank players, it is now accessible across 500 banks.

India

Real-time transactions

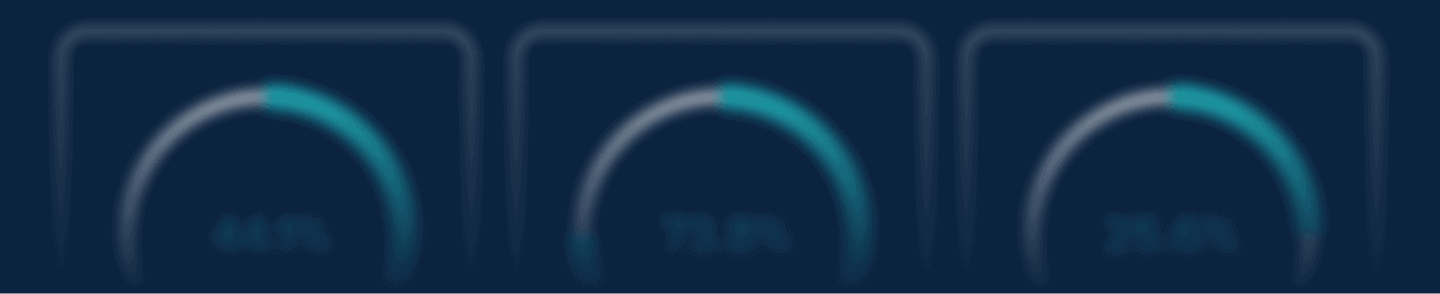

2023 Real-time share of electronic payments

84%

2028f

248.3B

2023-2028 CAGR

13.9%

Real-time payments launch

2010

Scheme messaging

ISO 8583

Real-time payment schemes

IMPS

2010

UPI

2016

New use cases broaden UPI reach and extend merchant opportunity

Recognizing that not all Indians have smartphones, UPI 123PAY provides access to real-time payments for the country’s 400 million feature phone users.

Users can set up real-time subscriptions for using UPI Autopay for recurring payments up to INR 2,000. Credit cards can also link to UPI, enabling acceptance at merchants that do not have POS terminals.

The next steps will be helping banks and fintechs to monetize services and rolling out low-cost, real-time corridors for remittances to capture higher-value payments.

CustomersPartners

CustomersPartners